Summary

First-generation LYTs were each built around a single yield engine, but this monolithic design breaks at scale because yield is cyclical to one regime, returns dilute as strategies hit capacity, and risk concentrates in a single failure mode, which is why the category is now shifting toward multi-source reserves.

Running an adaptive multi-source LYT requires three hard-to-build capabilities: cross-asset risk monitoring that treats heterogeneous sources on a common basis, rules-based governance with delegated execution that can rebalance faster than quarterly cycles, and direct access to yield sources rather than going through intermediaries.

Sierra is the case study for this shift, built multi-source from day one across DeFi, basis trades, and institutional RWAs via OpenTrade's source-agnostic vault infrastructure, signaling that the competitive moat is moving from yield strategy itself to the risk, governance, and access infrastructure underneath it.

1. The End of the Monolithic Era

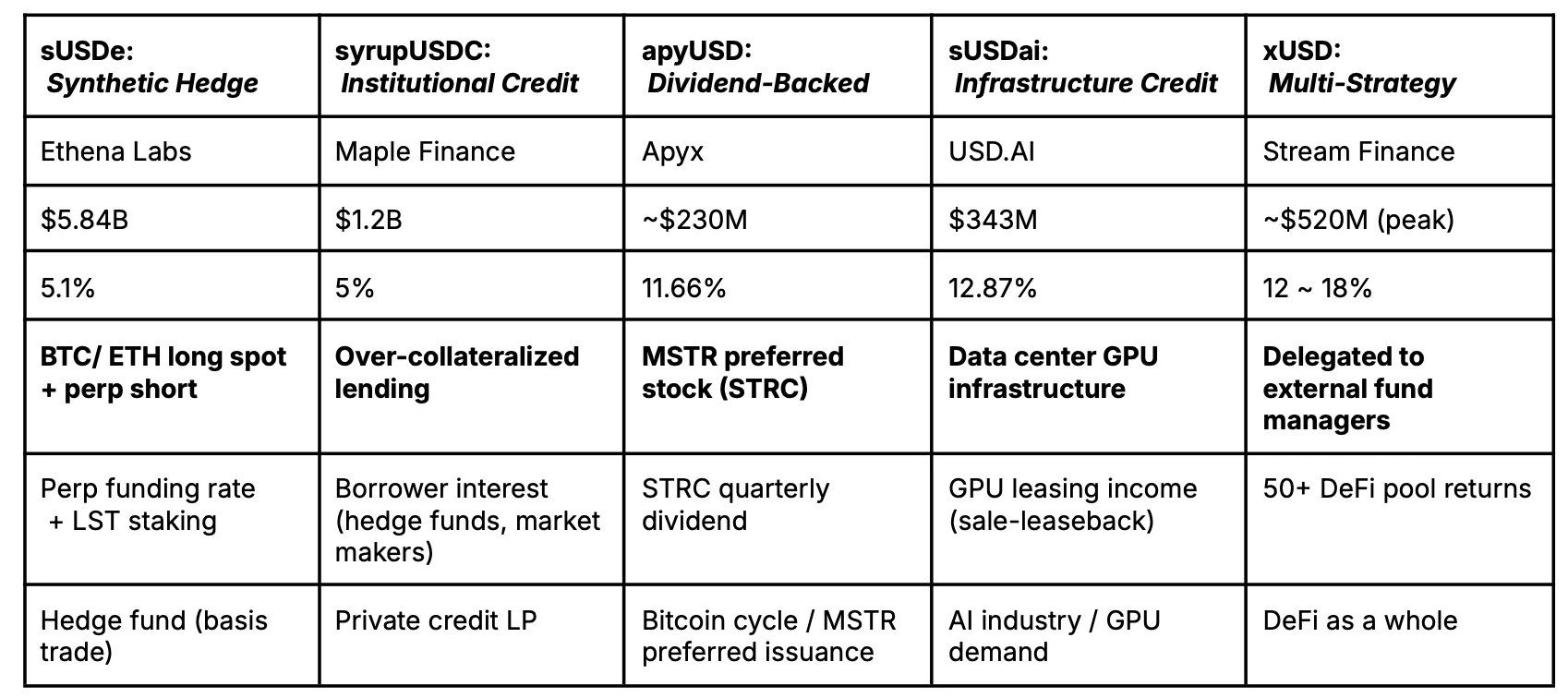

The first generation of Liquid Yield Tokens (LYTs) was organized around a single idea: find one inefficiency in capital markets, tokenize exposure to it, and scale. Ethena captured the perpetual futures basis trade. Maple packaged overcollateralized institutional lending. Ondo and Superstate brought tokenized Treasuries on-chain. Each protocol was, in effect, a wrapper around a single yield engine, and each scaled on the strength of that one strategy.

The category-defining incumbents are now visibly walking away from that pattern. Ethena has spent the past year diversifying USDe's backing into stablecoin lending, tokenized Treasuries, institutional loans, and most recently AAA-rated CLOs and equity-and-commodity perp strategies. The shift was not optional. Basis trade capacity ran out faster than capital flowed in, and the team chose diversification over a hard ceiling on AUM. Maple is making a parallel move, expanding its credit surface beyond pure overcollateralized lending into broader credit products and adjacent yield primitives.

This is not a failure of any particular strategy. The basis trade still works when funding is positive. Overcollateralized institutional lending still works when crypto-native borrowers want leverage. Treasuries still pay the risk-free rate. The problem is that any single-source yield token is structurally fragile in a way that only becomes visible at scale, and the market has now run that experiment with public results.

The interesting question has shifted. It is no longer which yield source wins. It is which issuers are architected to rotate across all of them. Call it the adaptive turn.

Figure 1: LYT Issuers by Strategy, Scale, and Yield Profile

Source: DefiLlama, Presto Research

2. Why Monolithic Breaks

A single-source LYT has three structural problems that compound as it scales.

Yield is cyclical at the source. Every yield strategy in crypto is a bet on a specific market regime. The basis trade needs funding rates to stay positive. Overcollateralized institutional lending depends on crypto-native borrowers wanting leverage. Even tokenized Treasuries move with whatever the Fed decides to do. No single yield source works in every regime. So every monolithic LYT has a yield curve that looks like the P&L of the one strategy it runs.

Figure 2: Basis Trades Falter in Bear Markets

Source: Coinglass

Scale dilutes the returns. The basis trade is limited by open interest and by how much size you can deploy without pushing funding against you. Overcollateralized lending is limited by the number of creditworthy institutional borrowers, which is smaller than most lending protocols want to admit. Tokenized Treasuries can scale to any size, but the yield is the same everywhere, so the only way to compete is on distribution. The bigger a monolithic LYT gets, the closer it gets to the ceiling of its own strategy, and the more its yield compresses at the margin.

Risk concentrates in one failure mode. A monolithic LYT has one dominant risk by design. For basis protocols, it is funding inversion and exchange counterparty risk. For lending, it is borrower quality and liquidation mechanics. For Treasury-backed tokens, it is custody and settlement risk. A reserve built around one strategy inherits the failure pattern of that strategy. Spreading across counterparties inside a single strategy helps a little, but the protocol's fate is still tied to one market.

These problems are manageable on their own at moderate size, and unmanageable together at scale. The drawdown across LYTs after October 2025 made this clear. The protocols that had grown fastest on a single-strategy yield saw the sharpest capital flight when that strategy came under pressure. A diversified reserve is not a nice-to-have for a mature LYT. It is a requirement for surviving the next regime change. The multi-source approach is the category's attempt to solve all three problems at once. The question is not whether to build adaptively, but what adaptive design actually requires.

3. What Adaptive Design Actually Requires

The capabilities needed to run a multi-source LYT at scale are worth stating plainly. The three features below are all necessary, listed in order of how hard they are to build for monolithic LYTs transitioning to the adaptive model:

Real-time risk monitoring across different asset types. A perp position does not fail the same way a CLO tranche depreciates, and neither fails the same way a DeFi lending market does. A multi-source protocol needs a framework that monitors each source on its own terms and still produces a single view of portfolio risk at the top. Frameworks built for one category and stretched to cover others tend to produce stitched-together risk bands rather than a coherent picture. A framework built to handle all categories from the start looks structurally different.

Governance that moves faster than a committee schedule. The day-to-day work of a multi-source protocol is constant reallocation. A quarterly governance cycle does not fit the architecture. But fully discretionary allocation breaks the trust properties that make an LYT usable as money. The answer is a rules-based framework with delegated execution inside set bounds. A board or risk council sets the allocation envelope, and the operational team reallocates within it. Reallocation is also only real if positions can be exited on the schedule the framework requires. That means reserves deployed into yield sources with short duration and contractual liquidity, not reliance on secondary markets.

Direct access to yield sources. Most DeFi protocols that touch RWAs today reach them through intermediaries. Centrifuge is the main one, wrapping credit and structured products into DeFi-ready vaults. Intermediated access has three structural costs: a fee layer, a limited menu of sources the aggregator has chosen to wrap, and a speed limit tied to the aggregator's own operations. None of these is a problem for a small static RWA allocation. All of them become a problem for a strategy built on continuous rotation. Direct access means a structural relationship with an institutional asset manager, set up around what a DeFi protocol actually needs to operate. It removes these costs and opens up the full institutional yield universe, not just the part that has been wrapped for DeFi.

Each of these capabilities is ordinary in institutional asset management. Putting all three together in one DeFi-native protocol is not. As LYTs evolve from monolithic to multi-source, competitive advantage evolves away from the underlying strategy itself, which likely becomes commoditized over time, and towards all of the infrastructure underpinning the LYT.

4. Sierra as a Case Study

Sierra is a useful example that demonstrates how an adaptive LYT has these capabilities implemented in practice. Its architectural choices are public, consistent with the framework above, and reflect decisions made from inception rather than arrived at through extension.

4.1. How Sierra Works

Sierra Protocol is a Liquid Yield Token issuance platform. SIERRA is the first LYT it has issued, a token whose value increases over time as the underlying reserves generate yield. The mint and redeem price rises each day reflecting the change in value of the underlying reserves. Authorized Participants arbitrage secondary markets against that increasing mint and redeem price, so SIERRA holders can sell their tokens for more than they paid, with accrued yield reflected directly in price rather than through staking or rebasing.

Reserves are deployed into vaults operated by OpenTrade, where each vault represents a single yield source. OpenTrade's vault infrastructure is yield source agnostic. The same operational layer can support DeFi exposures like Aave, Morpho, and Pendle PTs on EVM, Kamino or Figure's tokenized HELOCs on Solana, and a broad spectrum of RWAs including publicly traded funds with exposure to U.S. Treasuries, investment-grade commercial paper, and AAA-rated CLOs, as well as private funds issued by tier one asset managers.

This makes adaptive reserve management a property of the design rather than a periodic decision or protocol upgrade. New yield sources can be underwritten, wrapped into an OpenTrade vault, and added to the reserve, with daily rebalancing across the evolving set of yield sources in response to changing market conditions. The opportunity set expands continuously, and rotation across the existing set is operationally efficient.

4.2. Built Multi-Source From Day One

Ethena began as a pure basis trade wrapper and is now diversifying outward. Maple began as an overcollateralized institutional lending protocol and is extending into a broader credit surface. The direction of travel is correct and the execution is real. What neither protocol can erase is the architectural assumption of its original design. Risk frameworks were shaped around one yield source. Governance was built to adjudicate questions that used to have one answer. Token mechanics were designed for a single revenue stream. Every new yield category has to be reconciled against those commitments.

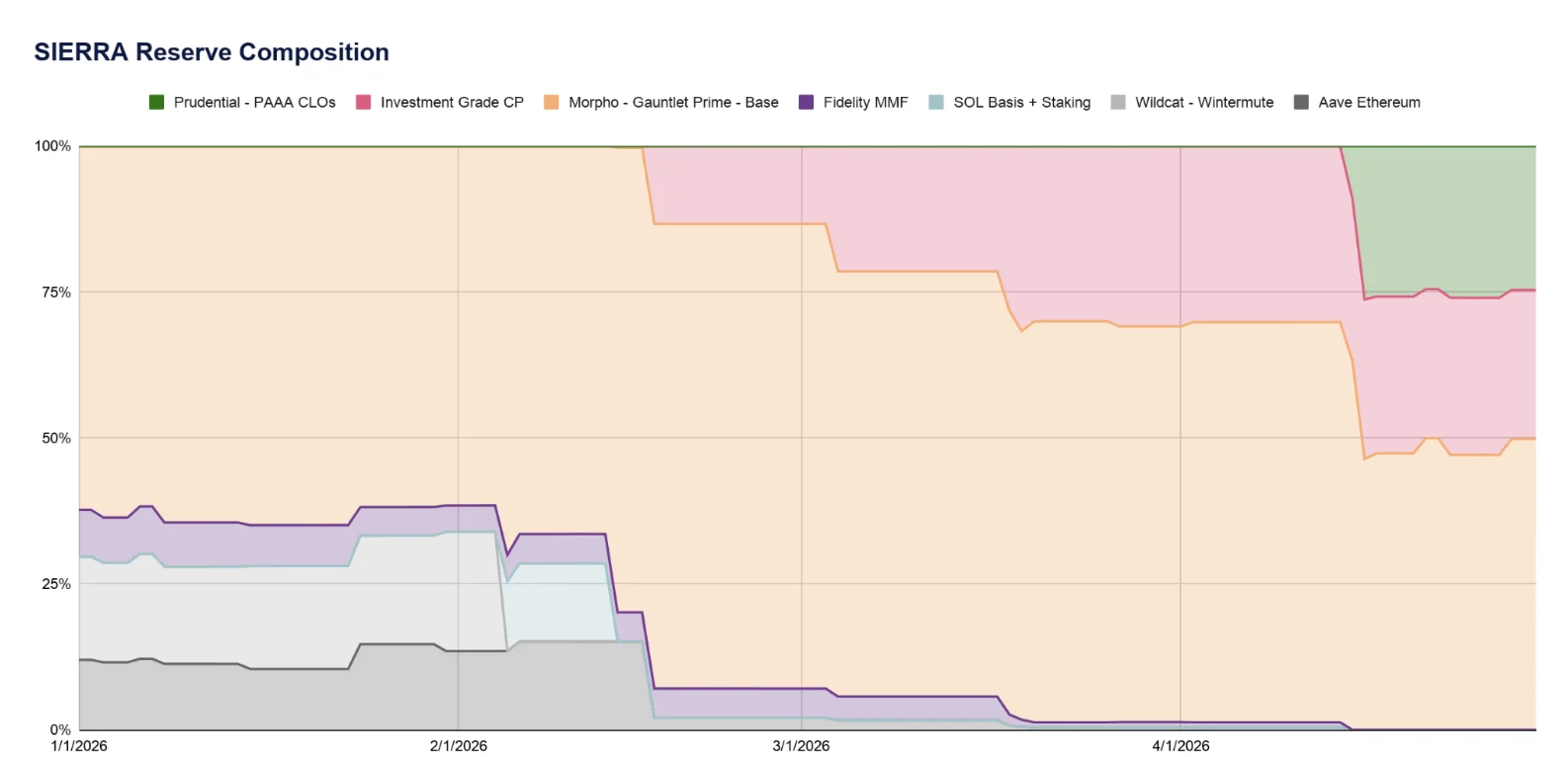

Sierra was built multi-source from the start. The reserve management strategy can span three categories rarely combined in a single LYT: blue-chip DeFi lending, delta-neutral basis strategies, and institutional-grade real-world assets. These three categories of yield sources are driven by largely uncorrelated factors and tend to offset each other during regime shifts, so a portfolio that holds all three yield across conditions is likely more resilient in comparison to an LYT backed by a single source that will inevitably compress.

Building this way from inception produces protocol architecture that retroactive changes to existing protocols cannot easily replicate. The risk framework is category-agnostic by default because it had to evaluate heterogeneous sources from day one. Governance relies on an Advisory Council that underwrites all yield sources and recommends adjustments, a structure built for the cadence of reallocation rather than periodic product changes.

Figure 3: Sierra's Reserve Composition

Source: Sierra

4.3. Direct Access to the Source

Direct access is the multi-source capability hardest to retrofit, and the RWA leg is where this plays out most visibly. Most DeFi protocols holding RWA exposure today reach it through Centrifuge-wrapped vaults. This is workable when RWAs are a side allocation but constrained when they are meant to serve as a structural counterweight to crypto-native yield.

Sierra reaches its RWA exposure exclusively through OpenTrade, an arrangement uncommon in the category. OpenTrade sources vaults with institutional counterparties, holds collateral in bankruptcy-remote accounts with Tier 1 institutions, and has those portfolios managed by an FCA-regulated asset manager. The arrangement bypasses the aggregator layer. Sierra's RWA opportunity set is the broader institutional yield universe, and its allocation can shift across sub-categories based on where risk-adjusted yield is best at a given moment. A protocol cannot rotate freely into a yield source it can only reach through an aggregator's limited shelf.

The same logic extends beyond RWAs. Because OpenTrade's vault infrastructure is source-agnostic, the access advantage applies equally to DeFi exposures across EVM and Solana and to structurally novel sources like tokenized HELOCs. The constraint that limits most DeFi protocols, being able to reach only what an aggregator has wrapped, does not bind here.

5. Implications

As monolithic LYTs continue to transition to the adaptive model, several clear implications emerge:

Yield profiles will converge. As protocols move to multi-source reserves, their yield curves start to look similar. The highs come down because no single strategy dominates. The lows come up because no single bad regime can sink the whole portfolio. The gap between protocols gets smaller over time, and investors start caring less about headline APY and more about risk-adjusted return. Protocols that keep marketing headline yield as their main selling point will fall behind where the category is going.

The moat moves to infrastructure. Yield strategy is becoming a commodity. Risk frameworks, governance, and access infrastructure are not. Analysts looking at LYTs should spend less time on headline APY and more time on these layers. The protocols that build a lasting edge over the next cycle will be the ones with better infrastructure for doing what everyone else is doing.

Architecture matters, but it is not everything. It is worth being clear about what adaptive design actually delivers. Distribution still matters. Ethena's deep integration across major DeFi venues is a real moat, and a new entrant with cleaner architecture will not attract capital just by showing up. Allocators also have a fair preference for simplicity. A single-strategy LYT is easier to underwrite than a multi-source portfolio that shifts every day. The argument for adaptive design is not that architecture beats everything else. It is that as strategy becomes a commodity, infrastructure decides more of the outcome. Native multi-source protocols are built for this shift. Retrofits are not.

The open question. Will multi-source design turn LYTs into commodities entirely, so that competition comes down to infrastructure, execution and distribution? Or will unique access and risk management create lasting differentiation? It is too early to say. What is clear is that the era of competing on yield strategy alone is ending.

6. Conclusion

For most of this cycle, the competition between liquid yield tokens was a competition between strategies. Protocols were identified with the trade they wrapped. Users picked a token the way they might pick a hedge fund.

That frame is dissolving. The protocols that grew largest on a single strategy are now diversifying away from it. The protocols emerging now are skipping that phase entirely and starting with multiple sources from day one. What both groups are converging on is not a better yield engine but a different product altogether: a portfolio held inside a token, managed against a clear set of constraints, designed to produce stable risk-adjusted returns across market conditions rather than peak yield inside a single regime.

This is a less exciting story than the one the category has been telling itself. The winning protocols will not be the ones with the cleverest trade. They will be the ones that built the least visible parts of the stack well: risk frameworks that treat heterogeneous sources on a common basis, governance that can act on the operational cadence the architecture requires, and access relationships that determine what the portfolio can actually reach. These capabilities are slow to build and hard to copy, which is why they are becoming the real basis of competition.

The adaptive turn is already underway. The question is which protocols are far enough along to compound a real lead before the rest of the category catches up.