Summary

Tokenization is climbing the asset-complexity curve, from stablecoins ($300B+) to tokenized Treasuries and now to equities, a $140T+ market that remains almost entirely on-chain-untapped today.

Securitize is the most fully regulated, vertically integrated tokenization platform, and its direct issuer-sponsored model, where the token is the real share rather than a wrapper, is the structure the SEC treats as most consistent with existing securities law, already proven at scale through BlackRock's BUIDL and now extending into equities.

Presto invested because value in tokenization accrues to the trusted, regulated infrastructure layer, much as it did for stablecoin issuers, and Securitize is furthest along that curve, making now the window to back the emerging category leader.

1. From Stablecoins to Equities

The tokenization of traditional financial assets has followed a predictable sequence. Each stage is governed by the complexity of the asset being brought on-chain.

Stablecoins came first. A licensed issuer custodies fiat currency and mints a 1:1 digital representation. The asset is simple, the rights are simple, and the regulatory pathway is now well defined. Stablecoin market capitalization exceeds $300 billion. The GENIUS Act, signed into law in July 2025, established the first federal framework for stablecoin regulation in the United States.

Tokenized U.S. Treasury funds came next. Products like BlackRock's BUIDL and Circle's USYC are money market funds whose shareholder registries are maintained on blockchain by SEC registered transfer agents. The underlying asset is standardized, the yield is predictable, and the compliance structure maps onto existing fund regulation without friction. The tokenized treasury market now represents several billion dollars in on-chain issuance.

Equities are the logical next step, and they are fundamentally harder. Stocks carry a complex bundle of rights: ownership, voting, dividends, governance participation. They trade across venues in different regulatory regimes. Their prices are volatile and venue dependent. The existing equity market infrastructure has been built over decades around brokers, clearinghouses, depositories, and transfer agents. It is deeply entrenched.

Figure 1: Benefits of Tokenization

Source: Securitize

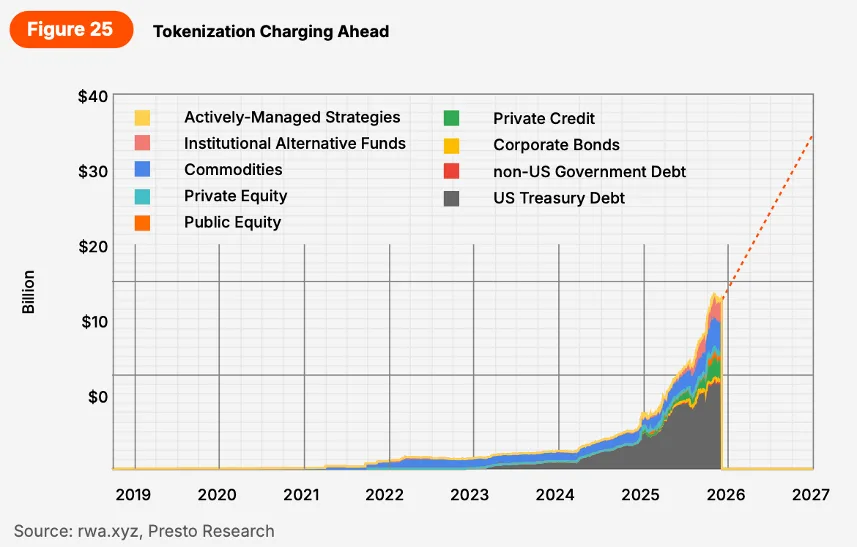

The numbers frame the opportunity. The global equity market exceeds $140 trillion. The U.S. alone accounts for roughly $72 trillion. Yet tokenized equity issuance remains under $2 billion. The question is not whether equities will be tokenized. It is who will build the infrastructure to do it at institutional scale, within the regulatory framework, and with the composability that makes on-chain assets genuinely useful.

Figure 2: Tokenization Charging Ahead

Source: rwa.xyz, Presto Research

2. What Securitize Actually Does

Securitize is an end to end tokenization platform. It manages the entire lifecycle of a digital security: issuance, investor onboarding, compliance enforcement, asset servicing, distribution, and secondary trading. Founded in 2017, it has assembled what is currently the only vertically integrated set of regulatory licenses for tokenized securities in the industry.

The first and most important license is the SEC registered transfer agent. In traditional equity markets, the transfer agent maintains the official shareholder registry on behalf of the issuing company. It updates records when shares change hands, identifies who receives dividends, and determines who gets to vote. Securitize performs this function using blockchain as the registry infrastructure. When a company tokenizes its stock through Securitize, the blockchain based record is the authoritative shareholder ledger. It carries the same legal weight as a traditional database maintained by Computershare. This is not a wrapper or a synthetic representation. The token is the share.

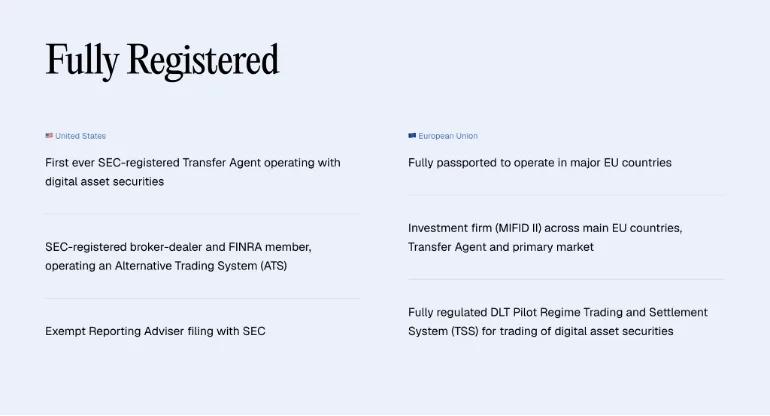

The remaining licenses complete the stack. The FINRA member broker dealer allows Securitize to distribute tokenized securities, custody investor assets, and act as placement agent for new issuances. The SEC regulated Alternative Trading System, called Securitize Markets, provides a venue for secondary trading through order book and RFQ mechanisms. The fund administration business handles NAV calculations, investor reporting, and operational management for tokenized funds. And the EU regulatory stack, comprising an Investment Firm license and a DLT Trading and Settlement System authorization passported across most EU jurisdictions, makes Securitize the only entity in the world licensed to operate regulated digital securities infrastructure in both the U.S. and the EU.

Each of these licenses took years of regulatory engagement to obtain. Assembled together, they create a compounding advantage for issuers who would otherwise need to coordinate across multiple service providers.

2.1. How It Works

These licenses define what Securitize is authorized to do. The DS Protocol is how it executes on-chain.

The DS Protocol is a blockchain native architecture for the regulated issuance and lifecycle management of digital securities. It consists of three components. DS Tokens are the tokenized securities themselves. DS Services include a Trust Service, a Registry Service, and a Compliance Service that collectively manage identity verification, ownership records, and transfer restrictions. DS Apps are third party applications that interact with tokenized securities through standardized interfaces.

The Registry Service maintains an on-chain record of every authorized investor. It maps wallet addresses to compliance attributes like accredited investor status and jurisdictional eligibility, populated after off-chain KYC verification through Securitize iD. Over 500,000 accounts have been registered through this system.

The Compliance Service is where the protocol's value becomes most apparent. Every time a DS Token is transferred, the Compliance Service checks whether the receiving address satisfies the issuer's rules. If the wallet is not registered, or if the transfer would violate holding limits, jurisdictional restrictions, lockup periods, or any other configured parameter, the transaction is blocked at the smart contract level. It cannot execute.

This is fundamentally different from indirect tokenization models. In those models, compliance is enforced only at mint and redeem. Once tokens are in circulation, on-chain transfers carry no compliance logic. The DS Protocol embeds compliance into the token's transfer function. The rules travel with the asset throughout its entire lifecycle, on any chain.

3. From BUIDL to Equities

The most instructive demonstration of this architecture in production is Securitize's partnership with BlackRock on BUIDL, the BlackRock USD Institutional Digital Liquidity Fund. Launched in March 2024 on Ethereum, BUIDL is a tokenized treasury fund that invests entirely in cash, U.S. Treasury bills, and repurchase agreements. Securitize serves as tokenization platform, transfer agent, and placement agent.

The mechanics illustrate the full stack in action. An investor subscribes through Securitize Markets after completing KYC through Securitize iD. Securitize creates a record of ownership on the blockchain. The fund mints BUIDL tokens to the investor's wallet. Daily accrued dividends are paid as new tokens each month. Investors can transfer tokens 24/7/365 to other pre-approved investors, with every transfer validated by the Compliance Service. Redemptions reverse the process: tokens are burned and proceeds distributed.

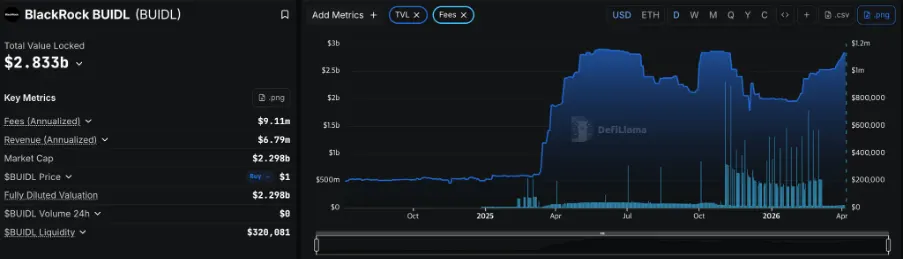

Within eighteen months, BUIDL became the largest tokenized treasury fund in the industry. It surpassed $2.5 billion in AUM and captured over 30% of the tokenized treasury market across more than forty competing products. The fund expanded from Ethereum to multiple additional networks including Arbitrum, Aptos, Avalanche, Optimism, Polygon, and Solana, with cross-chain interoperability powered by Wormhole.

Figure 3: BUIDL's TVL Has Been Growing Consistently

Source: DefiLlama

More importantly, BUIDL achieved real on-chain utility beyond buy and hold. It was accepted as off-exchange collateral on Binance. It was integrated into lending protocols including Aave. It backs stablecoins like Ethena's USDe. Major DAOs including Arbitrum and Sky (formerly MakerDAO) have allocated to it. And in February 2026, it was integrated into UniswapX for decentralized trading, marking BlackRock's first engagement with DEX infrastructure.

The extension to equities is the natural next step. The same architectural stack applies, and the first live example is Exodus Movement Inc. (EXOD), a blockchain software company whose common stock has been tokenized through Securitize.

The EXOD process works as follows. Investors register on Securitize and complete KYC. They instruct their existing brokerage to transfer EXOD shares via the Direct Registration System to Pacific Stock Transfer. Once confirmed, Securitize reflects the shares in the investor's account and issues corresponding on-chain tokens. The investor is the direct owner. Their name appears on the issuer's official shareholder registry. They receive all rights: ownership, voting, dividends.

This direct tokenization model is what the SEC has supported as the most compliant approach. In a January 2026 statement on tokenized securities, the SEC classified it as Issuer Sponsored Tokenized Securities and confirmed that it raises no novel regulatory concerns. By contrast, the SEC cautioned investors about indirect models where a third party purchases shares and issues derivative tokens, noting that holders in those structures have no direct rights in the underlying shares.

This distinction gives Securitize a structural advantage. Ondo Finance, the largest tokenized securities platform by total value locked with over $2 billion, uses an SPV to purchase stocks and issue wrapper tokens. This scales quickly but holders have no direct ownership or voting rights. Backed Finance, recently acquired by Kraken, follows a similar wrapper model under the Swiss DLT Act. On the infrastructure side, DTCC and Nasdaq are both pursuing blockchain based tokenization within their existing systems, bringing massive liquidity pools but taking incremental approaches rather than building new architecture. The addressable opportunity is large enough to support multiple models. But for issuers who require full legal ownership transfer and complete regulatory compliance, Securitize is the only platform that offers the direct tokenization model with the full regulatory stack and proven production infrastructure.

4. Why Presto Invested

Presto's investment in Securitize reflects a conviction that the tokenization of financial assets will be massive, and that there is a meaningful first mover advantage for the platform that establishes itself as the trusted infrastructure layer early. Stablecoins demonstrated this pattern clearly. Tether and Circle became the dominant players not because they had the best product features but because they established the trusted issuance and redemption infrastructure that everything else relied upon. The same dynamic will play out in tokenized securities. Securitize is further along the infrastructure curve than any competitor.

The regulatory moat is the most durable element of the thesis. The combination of U.S. and EU licenses under a single platform is unique. The time and capital required to replicate it create a meaningful barrier to entry. As regulation continues to crystallize through instruments like the CLARITY Act, the SEC's formal classification of tokenized securities, and the DTCC's no-action letter, the premium on operating within the regulated framework will only increase.

Figure 4: Regulatory Moat of Securitize

Source: Securitize

The network effects are compounding. BlackRock's decision to use Securitize for BUIDL validated the platform for every subsequent institutional client. Apollo, KKR, Hamilton Lane, and VanEck followed. Each new partnership creates reference value for the next. Over 15,000 investors are active across the platform's products, and over 500,000 accounts exist through Securitize iD.

The revenue model captures value at multiple points in the tokenization lifecycle: issuance fees, transfer agent servicing fees, fund administration fees, ATS trading fees, and increasingly transaction based revenues from stablecoin conversions, dealer activities, and DeFi integrations. Revenue scales with both the stock of tokenized assets and the flow of activity around them.

The growth path follows a two stage logic. The near term focus is penetrating the existing crypto market, which exceeds $2 trillion in total capitalization, by growing tokenized fund AUM, launching new products with institutional asset managers, and expanding into tokenized public equities. The medium term objective is to reach TradFi investors with products that offer fractional ownership, lower minimums, and on-chain liquidity. If tokenized assets reach even a fraction of the $19 trillion TAM that BCG and Ripple project by 2033, the platform that holds 30%+ market share of tokenized funds stands to capture an outsized share of the resulting value.

5. Risks

Regulatory risk remains the most significant. While the current trajectory in both the U.S. and EU is favorable, tokenization sits at the intersection of securities law, banking regulation, and digital asset policy. A change in SEC leadership or an adverse enforcement action could slow adoption. Jurisdictional fragmentation could complicate the cross-border strategy.

Competitive risk is multi-dimensional. Nasdaq has filed for rule changes to support tokenized securities trading. DTCC received its no-action letter. NYSE is developing 24/7 tokenized trading capabilities. These incumbents bring massive existing liquidity pools and institutional relationships. At the platform level, well-capitalized competitors could attempt to build similar vertically integrated stacks, though the regulatory lead time provides meaningful protection.

6. Conclusion

Securitize has built what no other platform in the tokenization market currently offers: a vertically integrated, fully regulated infrastructure stack that covers the entire lifecycle of a digital security from issuance to secondary trading. The regulatory moat is deep. The institutional partnerships are validated by the largest names in asset management. The technical architecture embeds compliance at the protocol level rather than bolting it on as an afterthought. As 2026 shapes up to be the year equity tokenization moves from experimental to operational, Securitize is the platform best positioned to define how tokenized securities work at institutional scale. Presto's investment reflects a structural view that the infrastructure layer of this emerging multi-trillion dollar asset class will be the most durable source of value, and that the window to establish that position is now.